Most businesses do not think very deeply about payments when things are working normally. Customers complete checkout, orders move through the system, and revenue appears in dashboards. But the moment problems begin, payments suddenly become one of the most operationally sensitive parts of the business. Transactions fail without explanation, settlement delays create support tickets, and customers insist they already paid while systems still show pending transactions.

This is usually the point where businesses realize something important: online payments for businesses are not just checkout tools. They are infrastructure systems that connect customer behavior, operational processes, financial visibility, and revenue flow. As businesses expand across markets, devices, and payment environments, online payments increasingly become an operational challenge rather than a simple checkout function.

Online Payments Changed Faster Than Most Businesses Realized

For a long time, online payments were relatively predictable. A business integrated card processing, connected a payment gateway, and considered the payment problem mostly solved.

Modern ecommerce no longer behaves that way.

Customers now move across mobile devices, digital wallets, regional payment methods, subscription systems, invoicing flows, crypto networks, and real-time payment environments. These evolving payment behaviors continue to reshape customer expectations and operational requirements across digital commerce. A checkout experience that performs well in one market may create friction somewhere else. A payment method trusted in one region may feel unfamiliar in another. Even settlement expectations have changed. Businesses increasingly expect operational visibility immediately rather than days later.

This evolution changed the role of payments inside online businesses.

Payments are no longer isolated financial events happening at the end of checkout. They influence conversion rates, customer trust, operational workload, international scalability, retention, and even brand perception.

A slow or confusing payment flow can quietly damage sales even when the product itself is strong. A technically functional payment system can still create operational instability if transaction visibility is poor or settlement handling becomes difficult to manage at scale.

That is why businesses increasingly evaluate payments as infrastructure decisions rather than simple integrations.

Payment Methods Are No Longer Just About Convenience

One of the biggest misconceptions in ecommerce is the idea that offering more payment methods automatically improves performance.

In practice, payment methods only help when they align with customer expectations and operational reality.

A customer in one country may strongly prefer digital wallets. Another may trust bank transfers more than cards. Mobile-first buyers often behave differently from desktop buyers. Subscription businesses care deeply about recurring payment reliability, while digital product businesses may prioritize speed and simplicity above everything else.

This is why modern payment strategy is increasingly tied to behavioral understanding rather than payment quantity.

Businesses now evaluate payment methods based on questions like:

- Which methods reduce checkout abandonment?

- Which methods create the least operational overhead?

- Which methods customers already trust?

- Which methods settle efficiently?

- Which methods work reliably across multiple regions?

The answer is rarely universal.

Credit cards may still dominate globally, but local payment systems remain extremely influential in many regions. Digital wallets continue changing mobile checkout behavior. Stablecoins and blockchain payments are increasingly becoming operational tools for international businesses seeking faster and more direct settlement models.

The important point is not that one payment method replaces another.

It is that online businesses now operate in a fragmented payment environment where customer expectations vary significantly depending on geography, platform, industry, and payment context.

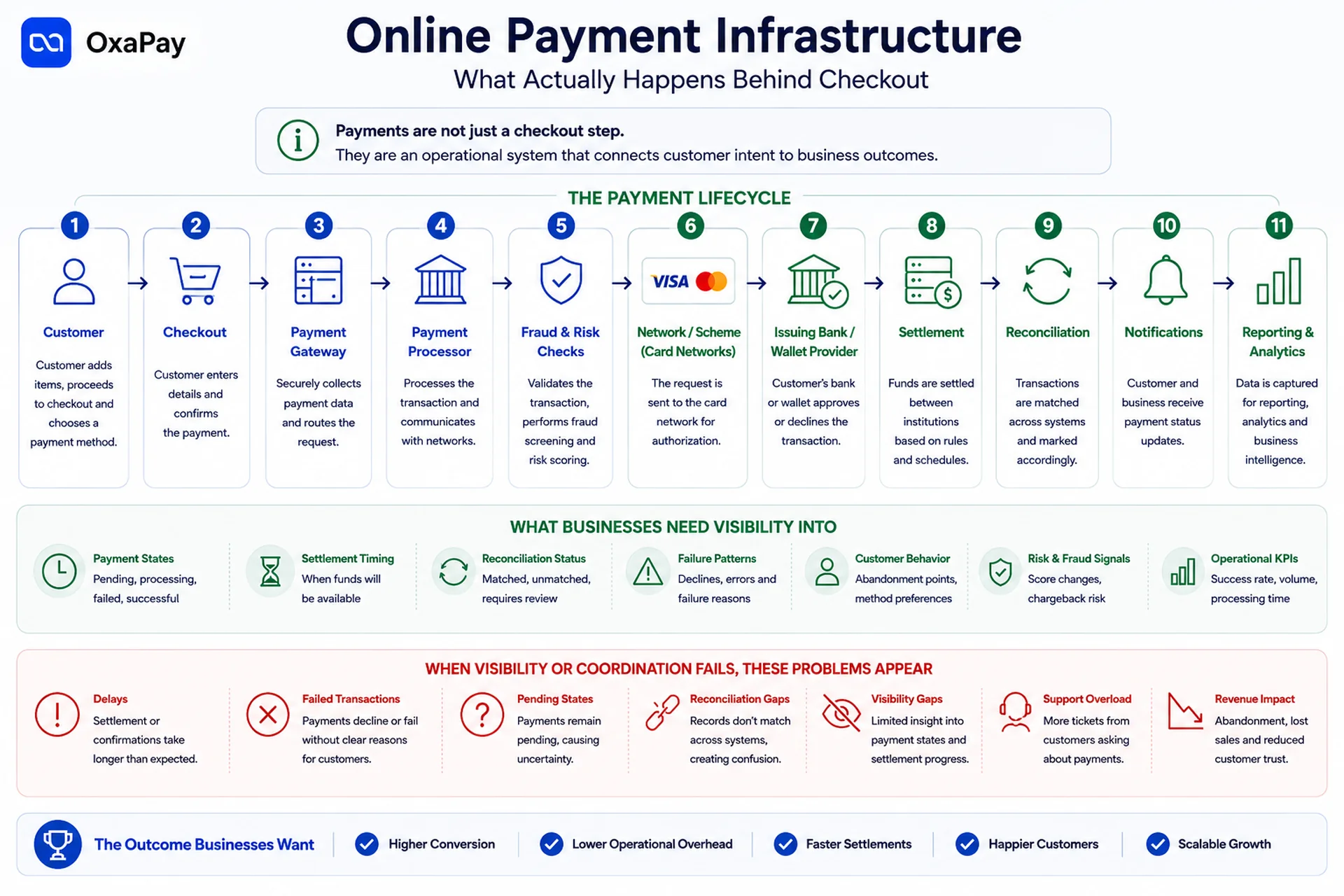

Behind Every Successful Payment Is an Operational System

Customers usually experience payments as a simple interaction.

They click a button, authorize the transaction, and expect confirmation.

Operationally, far more is happening behind the scenes.

Modern payment systems coordinate multiple layers simultaneously. Payment gateways, processors, fraud systems, settlement logic, transaction monitoring, reconciliation workflows, customer notifications, confirmation tracking, reporting systems, and industry payment security standards may all influence how a transaction moves through its lifecycle.

As businesses scale, these operational layers become increasingly important.

A small business handling a few transactions per day can manually investigate payment issues. A larger business processing thousands of transactions across multiple countries cannot rely on manual workflows for long.

This is where operational payment infrastructure becomes critical.

Payment Visibility Problems

Businesses increasingly need visibility into payment states rather than only final outcomes. They need to understand which transactions are delayed, which remain pending, which failed, which settled successfully, and which require customer communication or operational review.

The payment itself becomes only one part of a larger operational system.

This shift is subtle but extremely important.

Many Payment Problems Are Not Actually Checkout Problems

Many payment problems businesses experience are not actually checkout problems. They are visibility problems, reconciliation problems, communication problems, or workflow coordination problems that appear later in the payment lifecycle.

For example, a transaction may settle successfully at the processor level while the internal order system still marks the payment as pending because reconciliation failed between systems. From the customer’s perspective, the payment worked. Operationally, however, the order workflow is now broken.

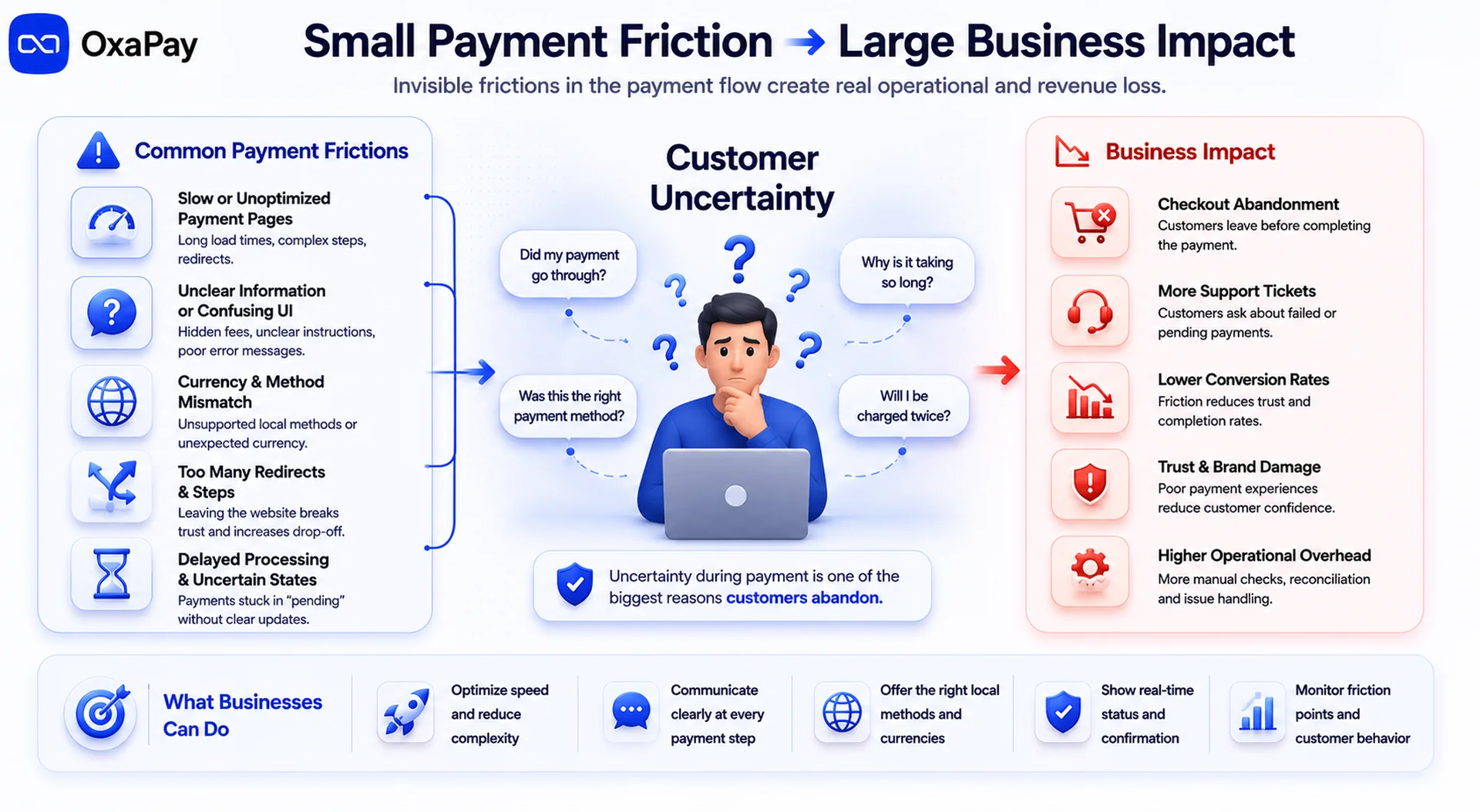

Why Payment Friction Quietly Reduces Revenue

Most customers will never explain why they abandoned checkout.

They simply leave.

Sometimes the cause is obvious, such as a failed transaction or unsupported payment method. But many forms of payment friction are smaller and harder to detect.

Small Friction Often Creates Larger Conversion Problems

A payment page loads slightly too slowly on mobile devices. A confirmation message feels unclear. Currency conversion appears unexpectedly late in checkout. A payment remains in “processing” status longer than the customer expected. The interface suddenly redirects through multiple unfamiliar pages.

None of these issues may look catastrophic individually.

Together, they create uncertainty.

And uncertainty is one of the biggest conversion killers in online payments.

This becomes especially visible in mobile checkout environments where even small payment delays or unclear processing states can cause customers to abandon the transaction before the payment lifecycle fully completes.

Trust Becomes Fragile During Payments

Customers become especially sensitive during payment because this is the moment where trust, money, and commitment intersect. Even technically successful payment systems can reduce conversion if the experience feels unpredictable or confusing.

International Payments Introduce a Different Level of Complexity

The operational difficulty of payments increases dramatically once businesses begin serving global customers.

Domestic payment systems are usually more predictable because customer expectations, currencies, banking rails, and settlement behavior remain relatively consistent. International commerce changes those assumptions and introduces a new set of cross-border payment challenges that businesses must address as they expand into new markets.

International commerce changes those assumptions.

Now businesses must consider:

- regional payment preferences

- localized checkout expectations

- settlement variability

- multi-currency handling

- transaction trust differences

- mobile payment behavior

- international payment reliability

- operational visibility across markets

Cross-Border Payments Create Operational Uncertainty

Cross-border transactions often introduce more uncertainty into the payment process itself. Settlement timing may vary. Approval behavior may become inconsistent. Customers may distrust unfamiliar payment experiences. Currency handling may create friction even before checkout completes.

A business selling digital products internationally may see a customer complete payment successfully while internal settlement visibility still remains delayed. Operationally, this creates uncertainty. The customer expects immediate delivery, while the business may still be waiting for confirmation that the payment can safely move into a completed state.

This is why global ecommerce increasingly depends on payment adaptability rather than payment availability alone.

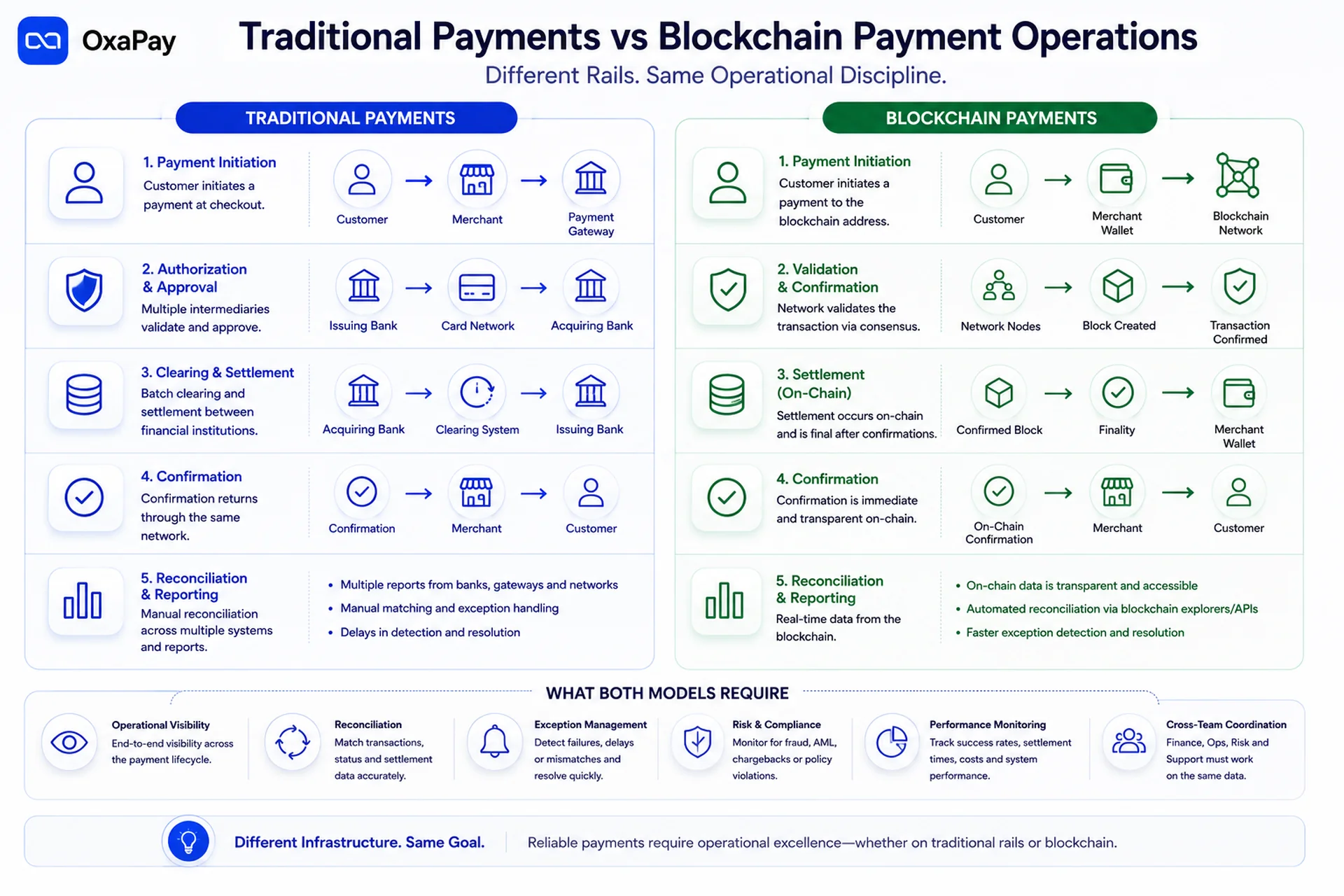

Blockchain Payments Introduced a Different Operational Model

Blockchain payments changed more than settlement speed.

They changed some of the assumptions behind online payment infrastructure itself.

Traditional systems usually rely heavily on intermediary coordination. Banks, processors, card networks, and financial institutions participate in transaction approval, settlement, and reversibility management.

Blockchain systems approach trust differently.

Transactions are verified through network consensus and cryptographic validation rather than centralized institutional approval. Operationally, this changes how payments move through the system.

Blockchain Payments Shift Operational Responsibility

But this does not make crypto payments “simpler” operationally.

In many ways, it shifts responsibility into different areas.

Businesses accepting blockchain payments must understand transaction states more carefully. A transaction being visible on-chain does not always mean it should immediately be treated as operationally final. Confirmation handling, invoice expiration, underpaid transactions, network selection, and transaction monitoring all become important parts of payment operations.

Confirmation Visibility Becomes Operationally Critical

For example, a business delivering digital services may detect a blockchain transaction almost instantly while still waiting for enough network confirmations before treating the payment as operationally safe. From the customer’s perspective, the payment already appears completed. Operationally, however, the business may still be managing confirmation risk behind the scenes.

This becomes even more important in high-volume environments where transactions arrive across multiple networks with different confirmation behavior, settlement characteristics, and operational risk profiles.

This is why modern زیرساخت پرداخت کریپتو increasingly focuses on payment state management rather than simple wallet connectivity.

The important operational layer is not only the blockchain itself. It is the coordination system built around blockchain transaction behavior.

Payment Coordination Matters More at Scale

As payment environments become more fragmented across traditional and blockchain-based systems, operational coordination becomes increasingly important for businesses managing payments at scale.

For online businesses, this becomes especially valuable when handling international transactions, digital products, subscription flows, or high-volume payment environments where manual monitoring is no longer practical.

Payment Visibility Is Becoming a Competitive Advantage

As payment systems become more complex, visibility becomes more valuable.

Businesses increasingly need to see what is happening operationally across the payment lifecycle rather than only receiving a final transaction result.

This includes understanding:

- payment states

- زمانبندی تسویه حساب

- failed transaction patterns

- customer payment behavior

- operational bottlenecks

- confirmation progress

- transaction anomalies

- recovery opportunities

Reactive Payment Operations Do Not Scale Well

Without visibility, payment operations become reactive.

Teams spend more time investigating problems manually, resolving customer confusion, reconciling transaction mismatches, and handling support escalations.

This is one reason modern payment systems increasingly compete on operational intelligence rather than only transaction acceptance.

Businesses now expect dashboards, transaction tracking, automated callbacks, reconciliation support, analytics, and real-time operational monitoring as normal infrastructure capabilities.

The payment layer is becoming deeply integrated into operational decision-making itself.

Online Payments Are Becoming Strategic Infrastructure

One of the most important changes in modern ecommerce is that payment systems are no longer purely financial tools.

They are operational systems with direct influence on growth.

Payment Systems Now Influence Business Growth

A payment system influences how quickly customers trust the checkout experience, how efficiently businesses handle operations, and how easily companies expand across international markets. It also shapes retention, conversion rates, support workload, and long-term scalability.

This changes how businesses evaluate payment decisions.

The question is no longer simply:

Can this provider process transactions?

Modern businesses increasingly ask:

Can this payment infrastructure support long-term operational growth without increasing friction for customers or complexity for internal teams?

That is a very different type of decision.

And it reflects how central payments have become to modern digital business itself.

نتیجهگیری

Online payments for businesses are no longer isolated financial events sitting at the edge of checkout. They increasingly shape how businesses operate internally, how customers experience trust during transactions, and how companies scale across markets, payment environments, and operational systems.

As payment ecosystems become more fragmented across regions, devices, networks, and settlement models, the real challenge is no longer simply accepting payments. It is coordinating visibility, operational reliability, transaction interpretation, and customer experience across increasingly complex payment flows. In modern ecommerce, payment infrastructure has become part of the operational architecture of the business itself, particularly for companies building scalable business payment infrastructure across multiple markets and payment environments.